M&A Issues: Timing

Yet another post in the M&A Issues series. This one is about timing, ie how long it should take from the first serious conversation about a sale transaction until the closing.

I’ve seen acquisitions done in a week. I’ve seen acquisitions take over a year from the first serious conversation to close. And one thing I know for sure, if a buyer wants to take their time and feels like they can get away with it, they will.

Not every buyer wants to take their time. Many buyers want the transaction closed as soon as possible. In that case, the seller has alignment with the buyer and the transaction closes quickly.

Sellers usually want a quick close. They should. Selling your business is distracting and fraught with risk. One you decide you are going to sell, you should move with as much speed as you can while being diligent, thorough, and reasonable.

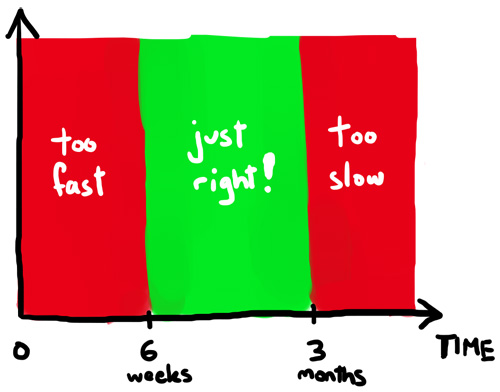

Six weeks from serious conversation to close is fast. If the company is “clean” and the buyer is incented to do a quick close and there are no governmental approves, it can be done.

Anything over three months is too long. The sale process starts to hang over the company and impacts the team, the business, and can lead to lasting problems. Team members get antsy. Resumes hit the street. Customers hear rumors and start thinking about plan B. The senior team loses focus. The company suffers.

If there are reasons why a close is going to take a long time (governmental approvals, buyer approvals, diligence, etc) an approach you can take is to sign a defintive agreement which obligates both sides to close and provides remedies if the close does not happen (including breakup fees). This is often the way deals are done with public companies that require shareholder approval.

Another key issue related to timing is the news leaking out. The longer the process goes on, the more likely the news will leak out. The reality is most deals leak and it rarely gets in the way of a deal getting done. Buyers hate it when the news leaks out because it can bring additional buyers into the process and make it more competitive. But most sellers should prefer a quiet process too. The less chatter about the sale, the better in my opinion.

I’m a fan of quick M&A processes, within reason. It takes time to do the required diligence and legal work. Doing a deal in a day is generally not a good idea. Doing it in six weeks is desirable and should be the goal. Anything longer than three months is likely to be problematic and will require a ton of management effort to manage the fallout. If you are a seller, you should specifiy the time to closing in the LOI and do everything in your power to make the buyer meet that deadline. And if you are buyer, you should respect the seller’s desire for a quick close and work hard to make it happen on your end.

From the comments

JLM added: