Accounting

I’m making up the curriculum for MBA Mondays on the fly. The end game is to lay out how to look a businesses, value it, and invest in it. We started with the time value of money and interest rates, we then talked about the corporate entity. Now I want to talk about how to keep track of the money in a company. That is called accounting. This will be a multi-post effort and will include posts on cash flow, profit and loss, balance sheets, GAAP accounting, audits, and financial statement analysis. But before we can get to those issues, we need to start with the basics of accounting.

Accounting is keeping track of the money in a company. It’s critical to keep good books and records for a business, no matter how small it is. I’m not going to lay out exactly how to do that, but I am going to discuss a few important principals.

The first important principal is every financial transaction of a company needs to be recorded. This process has been made much easier with the advent of accounting software. For most startups, Quickbooks will do in the beginning. As the company grows, the choice of accounting software will become more complicated, but by then you will have hired a financial team that can make those choices.

The recording of financial transactions is not an art. It is a science and a well understood science. It revolves around the twin concepts of a “chart of accounts” and “double entry accounting.” Let’s start with the chart of accounts.

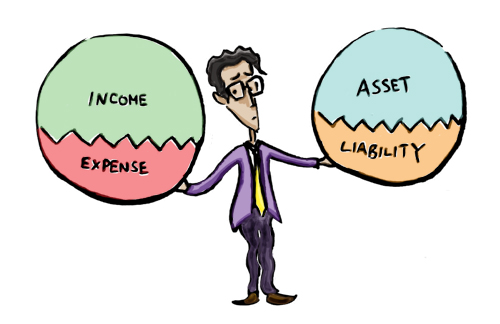

The accounting books of a company start with a chart of accounts. There are two kinds of accounts; income/expense accounts and asset/liability accounts. The chart of accounts includes all of them. Income and expense accounts represent money coming into and out of a business. Asset and liability accounts represent money that is contained in the business or owed by the business.

Advertising revenue that you receive from Google Adsense would be an income account. The salary expense of a developer you hire would be an expense account. Your cash in your bank account would be an asset account. The money you owe on your company credit card would be called “accounts payable” and would be a liability.

When you initially set up your chart of accounts, the balance in each and every account is zero. As you start entering financial transactions in your accounting software, the balances of the accounts goes up or possibly down.

The concept of double entry accounting is important to understand. Each financial transaction has two sides to it and you need both of them to record the transaction. Let’s go back to that Adsense revenue example. You receive a check in the mail from Google. You deposit the check at the bank. The accounting double entry is you record an increase in the cash asset account on the balance sheet and a corresponding equal increase in the advertising revenue account. When you pay the credit card bill, you would record a decrease in the cash asset account on the balance sheet and a decrease in the “accounts payable” account on the balance sheet.

These accounting entries can get very complicated with many accounts involved in a single recorded transaction, but no matter how complicated the entries get the two sides of the financial transaction always have to add up to the same amount. The entry must balance out. That is the science of accounting.

Since the objective of MBA Mondays is not to turn you all into accountants, I’ll stop there, but I hope everyone understands what a chart of accounts and an accounting entry is now.

Once you have a chart of accounts and have recorded financial transactions in it, you can produce reports. These reports are simply the balances in various accounts or alternatively the changes in the balances over a period of time.

The next three posts are going to be about the three most common reports;

- the profit and loss statement which is a report of the changes in the income and expense accounts over a certain period of time (month and year being the most common)

- the balance sheet which is a report of the balances all all asset and liability accounts at a certain point in time

- the cash flow statement which is report of the changes in all of the accounts (income/expense and asset/liability) in order to determine how much cash the business is producing or consuming over a certain period of time (month and year being the most common)

If you have a company, you must have financial records for it. And they must be accurate and up to date. I do not recommend doing this yourself. I recommend hiring a part-time bookkeeper to maintain your financial records at the start. A good one will save you all sorts of headaches. As your company grows, eventually you will need a full time accounting person, then several, and at some point your finance organization could be quite large.

There is always a temptation to skimp on this part of the business. It’s not a core part of most businesses and is often not valued by tech entrepreneurs. But please don’t skimp on this. Do it right and well. And hire good people to do the accounting work for your company. It will pay huge dividends in the long run.

From the comments

JLM said:

I am a firm believer that all businesspersons have to become 360 degree professionals. We have to be proficient on a great number of things. Accounting is one of those things. This is why you are the boss.

When starting out, get a CPA (small shop preferably) to set up your books on QuikBooks. He will already have the software and will undoubtedly have an existing client. This will take him about 15 minutes. Check, doublecheck and re-check the chart of accounts and the work product to be delivered.

You need at minimum — general ledger, financial statements (income statement, balance sheet, statement of cash flows), transaction journals (accounts receivable, cash receipts journal, accounts payable, cash disbursements journal, check register), payroll, bank reconciliations, debt reconciliation and a cash account reconciliation (only because cash is so dear).

Don’t panic, these documents are all produced by the software. All you have to do is bring him the invoices and he will cut the checks and you will sign the checks. At the startup phase, never, ever, ever, ever delegate check signing to anybody.

Feel the cash flowing through your fingers. This is like feeling a big fat Rainbow Trout “mouthing” your fly. It is the difference between landing the big one and well, not landing the big one.

For the first few months, have the CPA go over each and every document and explain them to you so you can see the linkages. You are in school now but it will only take an hour a month. In three months you will be an expert.

Then, get a bookkeeper or retain a bookkeeping service (small shop w/ lady w/ blue hair who does not smoke and has grandchildren and reminds you of your own grandmother — she will not embezzle from your accounts) and have them enter the transactions and have them reviewed and verified by the CPA on a monthly, quarterly and annual basis.

Maintain detailed files while requiring the CPA and bookkeeper to maintain the identical files.

As you grow, you will bring the bookkeeping in house and then the “controller” (CPA) function. In this way, you have developed a systematic approach which will be easy to assimilate and which will really change nothing as you grow. You will be growing “smooth”.

Last tip — have electronic access to your accounts at all times so you can check which things have been paid, which have not been paid (that’s sometimes how you manage cash flow — not paying on time) and how much cash you have.

Distribute the information to your key employees and partners/founders and make damn sure they read it. Overcommunicate.

You don’t want anyone to find out they are in a risky business when the first bomb goes off. Make them own the reality of the enterprise.

And Jon Smirl asked:

What level of disclosure to employees is appropriate? One startup I was in was damaged severely by the CEO keeping the books secret to himself. Since the books were secret we didn’t know when the company was running out of money, so we kept spending on a growth path. His plan was to raise more money before it ran out. He didn’t make it in time and we ran off a cliff. If we had known how tight the money was we could have adjusted spending. For example we bought a PBX right before we had to lay off a bunch of people.

JLM responded:

I have been running companies (private and public) for a long, long time. I have heard just about every compensation issue ever raised. I am not better for the experience, mind you, but it has made me adopt a policy which works very well for me.

I am not a Communist — though if I had been one I am convinced I would have been a very ruthless and good one.

I let everybody know everybody else’s compensation down to the salary, bonus, incentive comp, commissions, extra benefits (cars, vacation) level. Anybody can go to accounting and get the info at their own volition. They often do.

It saves a whole lot of problems in the long run and it keeps you on your toes. It makes you defend your own decisions and it makes you intellectually rise to the level of being perfectly rational.

It also sparks a dialogue from time to time that needs to be sparked. It also smokes out any bubbling personal discontent. You don’t want bubbling discontent. Lance the damn boil and deal with it in real time.

I once told a fellow who worked for me — who was very good but lazy as a dog — that he “could not hold another person’s jock”. He was mightily offended. I told him — “show me otherwise”. He did and I increased his compensation.

I only do and recommend stuff — even when it seems a bit weird and against my sometimes elitist instincts — because I know it works.

After more comments, JLM also revealed:

Everybody gets revealed and everyone can get all the info from the receptionist to the CEO. As CEO, I often don’t remember what folks get paid nor do I particularly care.

I always tell folks I am resposible for managing the company and they are responsible for managing their own careers. The first time I tell them that, they get a funny look on their faces. Then they get it. I am in the opportunity business not the fulfillment business.

I never really think about it until we make a bunch of money, then I give healthy bonuses — stock or cash. To everybody.

I am also very keen to make “tailor” made solutions. You have kids getting ready to go to college, I will dream up a college scholarship program. You are going to grad school at night, I will dream up a tuition reimbursement program — only if you make “A’s”. I make it up as I go and I don’t particularly worry about anything except SEC considerations.

I try to end up w/ a system wherein if the folks do well, I do very, very, very well. Has never failed me yet.

I have people who follow me from deal to deal because they know I will share the wealth. The greatest honor ever bestowed upon me in business is the high quality of folks who have invested their lives and confidence in me. It is really awe inspiring and I truly do not deserve it. It is the only real impediment to my working remotely from the mountains and Mexico 12 months of the year.

And along the way, I have a whole lot of damn fun. But I digress, sorry.

This post was originally written by Fred Wilson on March 8, 2010 here.