How To Calculate A Return On Investment

Originally published Jan 25 2010.

The Gotham Gal and I make a fair number of non-tech angel investments. Things like media, food products, restaurants, music, local real estate, local businesses. In these investments we are usually backing an entrepreneur we’ve gotten to know who delivers products to the market that we use and love. The Gotham Gal runs this part of our investment portfolio with some involvement by me.

As I look over the business plans and projections that these entrepreneurs share with us, one thing I constantly see is a lack of sophistication in calculating the investor’s return.

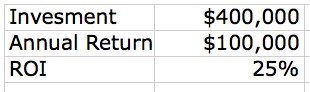

Here’s the typical presentation I see:

The entrepreneur needs $400k to start the business, believes he/she can return to the investors $100k per year, and therefore will generate a 25% return on investment. That is correct if the business lasts forever and produces $100k for the investors year after year after year.

But many businesses, probably most businesses, have a finite life. A restaurant may have a few good years but then lose its clientele and go out of business. A media product might do well for a decade but then lose its way and fold.

And most businesses are unlikely to produce exactly $100k every year to the investors. Some businesses will grow the profits year after year. Others might see the profits decline as the business matures and heads out of business.

So the proper way to calculate a return is using the “cash flow method”. Here’s how you do it.

- Get a spreadsheet, excel will do, although increasingly I recommend google docs spreadsheet because it’s simpler to share with others.

- Lay out along a single row a number of years. I would suggest ten years to start.

- In the first year show the total investment required as a negative number (because the investors are sending their money to you).

- In the first through tenth years, show the returns to the investors (after your share). This should be a positive number.

- Then add those two rows together to get a “net cash flow” number.

- Sum up the totals of all ten years to get total money in, total money back, and net profit.

- Then calculate two numbers. The “multiple” is the total money back divided by the total money in. And then using the “IRR” function, calculate an annual return number.

Here’s what it should look like:

Here’s a link to google docs where I’ve posted this example. It is public so everyone can play around with it and see how the formulas work.

It’s worth looking for a minute at the theoretical example. The investors put in $400k, get $100k back for four years in a row (which gets them their money back), but then the business declines and eventually goes out of business in its seventh year. The annual rate of return on the $400k turns out to be 14% and the total multiple is 1.3x.

That’s not a bad outcome for a personal investment in a local business you want to support. It sure beats the returns you’ll get on a money market fund. But it is not a 25% return and should not be marketed as such.

I hope this helps. You don’t need to get a finance MBA to be able to do this kind of thing. It’s actually not that hard once you do it a few times.

Additional notes

IRR is according to Wikipedia:

The internal rate of return (IRR) or economic rate of return (ERR) is a rate of return used in capital budgeting to measure and compare the profitability of investments. It is also called the discounted cash flow rate of return (DCFROR) or the rate of return (ROR).

From the comments

kidmercury asked

how seriously do you take these types of projections? to me financial forecasting for startups seems especially difficult. perhaps it is just me but i definitely don’t know how any entrepreneur can do it with any type of confidence/certainty. as an investor, do you find these types of projections to be useful?

RichardF followed up

Revenue predictions, in my experience, for a tech start up (or biotech for that matter) are really like waving a finger in the air. They are not even educated guesses. Particularly in years 3 and beyond when most people really start to ramp up the revenue.

I’d like to know how much attention Fred pays to the financial forecasts, particularly the revenue element, that he sees when people approach him for backing at USV.

fredwilson replied

expense projections are important to me in our USV investments. revenue projections are meaningless until the business starts to have revenues.

This post was originally written by Fred Wilson on January 25, 2010 here.